Media Contact

Kathy King

kingk@folioinvesting.com

703-245-4892

Folio News

2010

Socially Responsible Investing Made Simple

(by Jerilyn Klein Bier, Financial Advisor)

November 1, 2010 — Keeping up with clients’ SRI preferences can be very time consuming. Rather than go it alone, a growing number of SRI and mainstream advisors are turning to a platform offered by Folio Institutional. more

You don’t have to spend much time observing the sustainable and socially responsible investing world to realize that green comes in unlimited shades and sizes. There are small investors with huge appetites for responsible investments and large ones with more limited interest. Some advisors have built their practices around green, while others only stumble upon it occasionally.

No matter how green you or your clients may be, accounting for their preferences and needs on an account by account basis, and keeping up with any changes, can be mind boggling and very time consuming. Rather than go it alone, a growing number of SRI and mainstream advisors are turning to a platform offered by Folio Institutional.

With Folio, advisors can set up the same model portfolios for their SRI and regular clients. Client-selected exclusions coded at the account level automatically keep individuals away from any investments they wish to avoid and allocate their assets to other securities. Exclusions are based mostly on Standard Industrial Classification (SIC) codes, but also other sources such as the nonprofit Genocide Intervention Network.

“We sit under a whole bunch of SRI platforms. We’re the Intel inside,” says Greg Vigrass, president of Folio Institutional, a division of online brokerage Foliofn Investments Inc.

SRI has been part of the Folio platform since its inception nearly a decade ago, but its capability has evolved considerably, says Vigrass. Over the last couple years of market uncertainty and volatility, a growing number of investors have turned on SRI exclusions and other exclusions. Military weapons and firearms has been the most commonly used screen, followed by nuclear power, investments requiring a Schedule K-1 filing, alcohol, tobacco, gambling and genocide. K-1 tax requirements can be difficult and expensive to tackle.

Folio learned a lot about SRI from the First Affirmative Financial Network (FAFN), an independent registered investment advisor that specializes in serving socially responsible investors, says Vigrass. FAFN, which supports a nationwide network of investment professionals, has been using the Folio platform for about eight years.

“We were one of the early swimmers to jump in that pool. We kind of brought Folio up the SRI learning curve,” says FAFN president Steve Schueth. FAFN, which does its own SRI screening and also relies on screens from such SRI investment managers as Trillium Asset Management and Boston Common Asset Management, uses Folio as an administrative platform. FAFN can expose clients to a mix of managers and styles through model folios for a significantly lower minimum investment than if a client set up a traditional account with just one of those managers.

“The platform offers us a unified managed account platform typically not available in the SRI world,” says Schueth. The paperless system is also easy to use. “Advisors can move money back and forth with a few mouse clicks.”

SRI-focused investment advisory firm Azzad Asset Management, headquartered in the Washington D.C. suburbs, began using the Folio platform at the end of 2003 for its individual managed accounts. Azzad controls a model folio and whatever it specifies automatically impacts all subaccounts linked to that folio. Azzad president and CEO Bashar Qasem finds Folio’s platform very cost effective, simple and efficient. “Nobody has this; they’ve pioneered this.”

Whether an account has $10,000 or $1 million, Folio makes it possible for Azzad to give it the same treatment, says Qasem. Without the platform, it would be economically unfeasible to direct the same attention to smaller accounts. “Folio saves a lot of man hours,” he says. He also finds it very desirable from a compliance point of view. In addition to social screens, Azzad has clients who use Folio’s K-1 screens.

Sopher Investment Management, a Burlington, Vt.-based independent wealth manager, has been a Folio client for about a year. More than half of Sopher’s clients are interested in SRI. Some are actively seeking out SRI companies; more are looking to exclude companies. “Each client has their own thoughts on what socially responsible is. Meeting them can be challenging without a tool like Folio that can help manage different expectations,” says Sopher portfolio manager Matthew Johnson, CFA.

Johnson likes that Folio enables his firm to efficiently execute its strategy and manage accounts at one level but still meet individual preferences. It’s also cost effective for clients. Rather than paying per trade, they pay a flat fee for unlimited trading. Clients can also purchase fractional shares, making it much easier to offer smaller accounts diversification. Sopher has mainly relied on Folio’s screens, which Johnson says are very helpful. Sopher is also developing its own screens.

close

Folio Institutional Launches Online Marketplace for Advisors

(by Melanie Waddell, AdvisorOne)

October 4, 2010 — Custodial firm Folio Institutional, a division of online brokerage Foliofn Investments, has launched a new online marketplace called Model Manager Exchange that allows advisors working with the McLean, Va., based firm to access an initial 150 model portfolios from 35 financial professionals. more

“The Model Manager Exchange was designed to provide an easy way for advisors using the Folio Institutional platform to interact with one another and take advantage of a peer network that provides access to a collection of great thinking,” says Folio Institutional President Greg Vigrass. “Every advisor on our platform has access to an enhanced universe of innovative portfolio models created and managed by other advisors and institutions.”

Vigrass told AdvisorOne that Folio Institutional’s online exchange is ideal for advisors “on both sides of the fence: those that are looking to distribute their models, and those [advisors] that are looking to find other advisors on our platform who have specialties and expertise they can take advantage of.” Model Manager Exchange is also peaking the interest of firms that do not currently do business with Folio Institutional, Vigrass says, but “who are looking at the [online exchange] and saying, ‘I might want to start custodying some of my business at Foliofn if it means I can get access to some of these other portfolio managers.’ ” Other advisors are asking: “ ‘How do I get my models up there,’ ” Vigrass says.

Folios are customized baskets of securities which can be bought, sold or rebalanced in a single transaction. The Folio Institutional platform, the company says, “allows trading in fractional shares, so any dollar amount can be invested into a portfolio and spread across all of the holdings according to pre-set weights—regardless of per-share prices.”

Folio Institutional says it is initially offering Model Manager Exchange as a free service for all RIAs and broker-dealers who use its platform. Currently, there is no fee for advisors to display their models on the Exchange. However, the firm says that advisors who offer portfolio models are required to have a minimum level of assets on the Folio Institutional platform, with those funds invested in one or more of their models. Negotiations of licensing fees are conducted directly between the sellers and buyers of the investment strategies, Folio Institutional says.

Once a model is licensed for use, the firm says, “trades are executed via the Folio Institutional platform, which handles all back-office transactions between the licensor and licensee.”

close

Folio Institutional Launches Model Portfolio Service

(byDan Jamieson, Investment News)

October 1, 2010 — Folio Institutional has rolled out a service that allows its RIA clients to tap into model portfolios run by other advisers who hold assets in custody at the firm. more

The Model Manager Exchange has an initial group of 150 model portfolios from 35 financial professionals.

Folio initially is offering the exchange as a free service for all its 375 registered investment advisers, as well as the dozen broker-dealers who use its platform.

The firm doesn’t disclose assets run under the models, but Folio spokesman Mark Bagley said that 45 to 50 advisory firms have signed up to use portfolios run by other advisers since August, when the firm did a soft launch of the exchange.

“We expect that number to swell now that we’ve had the public announcement,” he said.

Many advisers who have their assets in custody at Folio were already doing subadvisory work for other advisers, said Greg Vigrass, Folio Institutional’s president. On the flip side, many advisers “were looking to use a subadviser or looking to outsource [investment management] to other entities,” he said, so the exchange “seemed like a natural fit.”

Mr. Vigrass said that the strategies used by Folio advisers run the gamut from traditional equity allocations to quant models, aggressive tactical models and income-producing strategies. Folio doesn’t disclose the assets that it has in custody, but the amount is in the “multibillions,” he said.

Parent company Foliofn Inc. was founded as an online discount brokerage in 1999 by Steven Wallman, a former commissioner at the Securities and Exchange Commission. The firm formalized its institutional business about seven years ago.

Mr. Vigrass said that assets held in custody by advisers now amount to about 75% of the firm’s total.

close

Folio Institutional Offers Expertise of Leading Managers via a New Online Marketplace

(by Nicole Bliman, Plan Sponsor)

September 29, 2010 — Folio Institutional is offering advisers access to the investment expertise of some of the industry’s leading portfolio managers via a new online marketplace. more

The “Model Manager Exchange” (MMX), currently features 150 portfolios from 35 financial professionals. Folio Institutional is initially offering the MMX program as a free service for all registered advisers and broker/dealers who use its platform.

Advisers wishing to have their models displayed can do so for free as well; however, they are required to have a minimum level of assets on the Folio Institutional platform, with those funds invested in one or more of their models.

Negotiations of licensing fees are conducted directly between the sellers and buyers of the investment strategies. Once a model is licensed for use, trades are executed via the Folio Institutional platform, which handles all back-office transactions between the licensor and licensee.

“MMX allows model managers to increase the reach and visibility of their portfolio strategies, while creating a new revenue stream for them,” said Folio Institutional President Greg Vigrass, in a press release. “Meanwhile, licensees can efficiently access third party expertise to offer their clients a broader range of managed investments.”

close

Model Manager Exchange Opens, Featuring 150 Portfolios from 35 Financial Professionals

(by Nicole Bliman, Plan Adviser)

September 29, 2010 — The “Model Manager Exchange” (MMX) currently features 150 portfolios from 35 financial professionals. more

Folio Institutional is initially offering the MMX program as a free service for all registered advisers and broker/dealers who use its platform. Advisers wishing to have their models displayed can do so for free as well; however, they are required to have a minimum level of assets on the Folio Institutional platform, with those funds invested in one or more of their models.

Negotiations of licensing fees are conducted directly between the sellers and buyers of the investment strategies. Once a model is licensed for use, trades are executed via the Folio Institutional platform, which handles all back-office transactions between the licensor and licensee.

“Effective today, every adviser on our platform has access to an enhanced universe of innovative portfolio models created and managed by other advisers and institutions,” said Folio Institutional President Greg Vigrass. “MMX allows model managers to increase the reach and visibility of their portfolio strategies, while creating a new revenue stream for them. Meanwhile, licensees can efficiently access third party expertise to offer their clients a broader range of managed investments.”

close

ETFs Shunned by Many Retirement Plans

(by Ari Weinberg, Registered Rep)

August 2, 2010 — Investment advisers are big fans of exchange-traded funds. But that often doesn’t extend to putting them on the menus of corporate retirement programs. more

The investing world’s current darlings, exchange-traded funds, get no love from 401(k) plans.

Investment advisers like ETFs for a bunch of reasons: They carry lower fees than most mutual funds, offer tax advantages and can trade like stocks. What’s more, an ETF price war broke out among big financial firms this spring—driving expenses and commissions even lower.

So why aren’t advisers, many of whom consult to corporate retirement plans, pushing to include ETFs in 401(k) portfolios? By the most generous estimates, only 5% of the $830 billion invested in ETFs is held within 401(k) plans.

Many advisers say the problem is simple: ETFs just aren’t a good match for 401(k)s. The big advantages that the funds offer get lost inside 401(k)s, these advisers say, and ETFs can bring technical headaches for the companies that manage the plans, so many don’t want to offer them.

No Cost Advantage?

Ary Rosenbaum, a retirement-plan lawyer in Garden City, N.Y., is among the skeptics. While he uses ETFs for his own investments, Mr. Rosenbaum says he can’t get the numbers for ETFs in 401(k) plans to add up. “Index mutual funds are already low cost,” he says, one reason they are popular in 401(k)s.

While ETFs can have similar or lower expenses—sometimes under 0.2% or even 0.1% of assets a year—investors generally must pay brokerage commissions to buy or sell them, unlike most funds in a corporate plan. (The total cost of a 401(k) plan can run above 1.5% of assets.)

Further, in a 401(k), investors typically won’t be able to take advantage of one of the key appeals of ETFs—the fact that they trade all day long rather than just once a day, as is the case for mutual-fund shares.

Likewise, Roger Wohlner, a Chicago-based financial planner, likes ETFs but hasn’t seen a reason to include them in the nine retirement plans he advises. While he generally recommends one or more index mutual funds to his clients, the ETF inclusion “feels like a solution looking for a problem,” he says.

Vanguard Group, which manages two of the 10 largest ETFs in the U.S., is of similar mind. In a September research note, the Vanguard Center for Retirement Research said that, while index ETFs may be a substitution for “high-cost actively managed funds,” in 401(k) plans, the true advantages of an ETF—intraday trading and tax efficiency—are less relevant to a tax-sheltered retirement account.

Tricky Proposition

ETFs add more complications. An ETF that tracks an index can see its price vary from the value of the underlying securities if the index is thinly followed or if there’s low demand for the ETF itself. Recent events have also set the ETF faithful back a few steps. More than two-thirds of the securities that saw aberrant trading during the May 6 “flash crash” were ETFs, for reasons that remain unclear.

Other Competitors

Those aren’t the only roadblocks ETFs face. Large corporate plans have access to the lowest-cost mutual funds, negating a large part of ETFs’ price advantage. They also have access to collective trusts—very-low-cost institutional accounts managed by banks.

At smaller companies, the obstacle is operating costs. Traditional mutual funds offer an easy way to pass costs along to participants: Many funds have special classes of shares for retirement plans that have extra fees built in to compensate advisers and service providers, as well as paying for record keeping and administration.

Such fees, including 12b-1 fees earmarked for marketing and distribution, can run to 0.5% or more of assets per year. ETFs generally don’t have 12b-1 fees, so they don’t offer that kind of bundling.

What’s more, it’s much tougher for third-party administrators of retirement plans to tackle trading and acquisition of ETF shares on behalf of the plan participants, as well as managing the record keeping for fractional-share ownership.

Cracking the Market

Still, a number of companies see opportunities to offer ETF-based 401(k) plans.

Darek Wojnar, managing director of product strategy for BlackRock Inc.’s BLK +0.45% iShares unit, the biggest issuer of ETFs, is working with third-party administrators to overcome the largest technical barriers to holding ETFs in the plans. So far, 60 administrators—in an industry of about 1,600 overall, according to Judy Diamond Associates—are set up to handle ETF transactions.

As for investor assets, iShares had $2.7 billion of its overall $352 billion in ETFs housed in 401(k) plans at the end of June.

In March, Folio Investments, Inc. launched Folio(k), a series of 401(k) offerings structured around ETFs. In the program—as with similar programs from other providers—participants can mix and match ETFs as they wish, or choose among portfolios of index ETFs in specific risk- or age-based allocations.

Several other firms, including ING Direct and Ascensus, are catering to plans looking to incorporate ETFs.

Some smaller players are getting in on the game, too. Brenda Wille-Cope, a managing partner at First Financial Strategies in Denver, moved her company’s own plan to risk-based ETF model portfolios constructed by 3D Asset Management of East Hartford, Conn.

Ms. Wille-Cope says the new plan has cut roughly a half percentage point from their retirement-investment costs. And “you see exactly what is charged against your account,” she says.

close

FOLIOfn to launch an online model portfolio exchange for advisers

(by Jessica Toonkel Marquez, Investment News)

July 15, 2010 — FOLIOfn Investments Inc. will launch an online model portfolio marketplace for financial advisers early next month. more

With more and more independent advisers selling model portfolios to other advisers, FOLIOfn’s new Model Manager Exchange gives sellers and buyers a clearinghouse in which to find and conduct business with each other, said Greg Vigrass, president of FOLIOfn Institutional.

For example, advisers who are looking for a small-cap-growth model portfolio will be able to search through a list of other advisers who offer this service, Mr. Vigrass said. FOLIOfn will do all the back-office work involved with transactions between sellers and buyers.

The exchange will initially feature 25 managers and about 75 models, “but we anticipate that number to increase quickly,” Mr. Vigrass said. There is no fee for firms to have their model portfolios listed, he said.

The firm however isn’t doing any due diligence on the managers other than basic screening, Mr. Vigrass said.

“We are not enforcing or recommending any of the managers or portfolios on the site,” he said.

Although other custodians such as The Charles Schwab Corp. allow advisers to tap other advisers’ model portfolios, the FOLIOfn service will actually handle the execution of the trades, making it easier for advisers selling their model portfolios to take on new clients.

“We make the changes to our model portfolio, and FOLIOfn executes the transactions,” said Dan Faucetta, a principal at Forefront Advisory, which will have two model portfolios on FOLIOfn. “For us, it’s a way of getting exposure and a way to bring our product to a lower break point of investors.”

Currently, Forefront’s model portfolios have a $500,000 minimum investment.

close

Folio(k) Retirement Platform Includes ETFs

(by Melanie Waddell, Investment Advisor)

April 1, 2010 — Hedge fund manager Joel Greenblatt and online brokerage pioneer Blake Darcy recently opened an online managed account service for retail investors. Can Greenblatt’s star power take asset management online? more

Folio Institutional, a division of online brokerage FOLIOfn Investments Inc., is furthering its foothold in the retirement planning space with the recent launch of Folio(k)—a 401(k) platform using target-date folios of exchange-traded funds (ETFs).

Folio Institutional, based in McLean, Virginia, has teamed up with Alliance Benefit Group Carolinas, a retirement plan recordkeeping and administration firm, to launch the Web-based Folio(k) platform. Participant enrollment, statements, investment requests, and employer reports are all delivered via the Internet.

Folio(k) is a turnkey 401(k) solution--including custody, trading, recordkeeping, and administration—and is available to advisors for a fee of 95 basis points.

“The retirement services space generally has been one of the fastest growing areas of our business,” says Greg Vigrass, president and CEO of Folio Institutional. “We’ve seen huge growth in advisors taking a fresh look at the [ETF] space, [and an] increase in the use of ETFs as the investment vehicle of choice, whether as an individual selection or building blocks of portfolios that advisors are using.”

Alan Smith, VP of retirement services at Folio Institutional, adds that “the interest in the Foliofn platform by RIAs has been growing by leaps and bounds, and we are introducing Folio(k) because of this and [to help] advisors to be competitive.”

Smith explains that plan sponsors as well as participants “are asking for more transparency, better diversification, and lower costs across the board.” That’s why Folio(k)’s “customizable portfolios of low-cost ETFs were developed with diversification and cost in mind. Participants actually own fractions of the underlying ETFs in a low cost, easy-to-use, Web-based 401(k). And fees can be deducted from plan assets, so there are no out-of-pocket expenses to the sponsor.”

According to Folio Institutional, the Target Date Folios reflect a far broader level of diversification than traditional target date funds, “which focus primarily or exclusively on domestic equities and fixed income and have proven to be costly and insufficiently diversified.” The Target Date Folios, include allocations to all the major asset classes. Moreover, the Target Date Folios are created with varying risk levels, including conservative, moderate, and more aggressive. Advisors, the firm says, may periodically rebalance account holdings and have the option of using Folio(k)’s updated model portfolio data as a resource. Advisors, Folio Institutional says, “can rebalance, add or delete securities, or change the weightings--easily across all accounts with one simple click. An entire basket of securities can be traded in one simple transaction with no commissions, transaction fees, or ticket charges.”

close

The Upstart Custodians

(by Jerry Gleeson, Registered Rep)

March 1, 2010 — Gordy Wegwart and his partners at Verity Investments were just about ready to give up. As Wegwart tells it, five years ago they had converted their broker/dealer practice in Durham, N.C., to an investment advisory practice and were looking for a new clearing and custodian service. more

It wasn’t a simple matter of going with a well-known national brand. Verity specializes in managing 403(b) retirement programs, and they were looking for a technology interface that would allow them to change the models for their clients’ asset allocations without incurring substantial trading costs. For nine months they examined dozens of custodians, culled from searches of the Internet and trade magazines and from conversations with industry colleagues. None of the companies had a system that exactly matched Verity’s needs.

“We found it was very difficult,” Wegwart says. “At one point we thought that it didn’t exist. We were about to throw our hands up and say, ‘What do we do now?’”

But they finally found what they were looking for — not at a goliath custodial firm but at a company in Colorado with a relatively modest $2.5 billion in assets.

In the custody and clearing world, giants still dominate. A survey of 100 registered investment advisors released in February by Morgan Stanley Research showed that just four companies accounted for 64 percent of assets custodied on behalf of RIA clients: Charles Schwab, Fidelity, Pershing, and TD Ameritrade. Schwab, the largest, reported $590.4 billion in custodied assets for its Advisor Services division at the end of 2009. Scale is critical to this business, because the greater the number of clients a company has, the more efficiently it can operate its pricey technology platforms, and the biggest players continue to grab market share. In their shadow are far smaller firms that are just eking out a profit, and scrambling to expand against significant odds.

“I don’t think the small players are winning,” says Tim Welsh, president and founder of California-based marketing researcher Nexus Strategy. “The 80-20 rule is alive and well in the industry, with 20 percent of the firms gathering 80 percent of the new assets. Small firms tend to stay small because they do not have any scale. Big firms can grow faster since they have infrastructure that can be leveraged with more clients and assets.” Also, custodial relationships tend to be “sticky.” Such tasks as paperwork, asset transfers, and the mastering of different software and computer systems can be daunting to advisors who might prefer to leave well enough alone.

Yet Welsh and other industry observers agree that opportunities exist for smaller firms in the clearing and custody channel that weren’t available years ago. Technology has become the great leveler in the financial advisory business, they argue, and business people who are adept can offer solutions that are tailored to the needs of an individual advisor at prices that are competitive with the large custodians. The need for custom-made solutions is likely to grow as the RIA channel itself expands and moves into niche markets, they say.

“I think that the big guys are vulnerable,” says Steve Winks, principal at srconsultant.com, an FA consultancy in Richmond, Va. “Because of their size, they're somewhat insulated from some of the factors that are driving the market. They don’t have to be responsive because they already are fairly dominant,” he says. But that leaves “the doors open for smaller custody firms that view disruptive innovation as the key to their winning market share.”

From Fledgling To Player

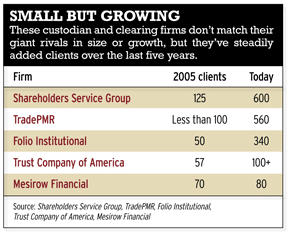

Some smaller custodians are setting themselves apart by providing extra high-touch client service. Patricia Heath, who has an RIA practice in Northfield, Ill., says she switched over to Shareholders Service Group about three years ago because she was impressed with the firm’s commitment to quality. One thing she noticed when she stopped by the company’s office to talk with management was a board on the wall that kept track of mistakes. The fact that they had a system in place to do so gave her a sense that attention would be paid to details, she says. It’s not unusual for her to put in 20 calls a day to her custodian on such matters as account transfers and issuing checks to clients. Before SSG, she had her share of instances where clients’ names were misspelled, mistakes that weren’t her fault but still reflected poorly on her. “A broker/dealer can make or break your business if they are sloppy or don’t get things done on time,” Heath says. “I’ve had clients for 20 years.”

Other small custodians compete by catering to the niche needs of smaller RIA firms. Wegwart sees his own experience as emblematic of that kind of market. “There’s definitely evolution going on in the industry,” he says. “Our business was built very much outside the box.” Wegwart’s Verity Investments custodies about $150 million in assets with Trust Company of America in Centennial, Colo., which provided the technology solution that Wegwart sought with such difficulty five years ago. A custodian that focuses on fee-based RIAs, Trust Company uses a technology platform that can roll up the multiple trades that portfolio rebalancing requires into a single trade, lowering trading costs to FAs and their clients, he says. Trust Company’s model seems to be working: Since Verity signed up in 2005, Trust Company’s assets have more than quadrupled to $9.1 billion. While it occupies the small end of the custodian size spectrum, continuing growth is very much on its agenda. Frank Maiorano, its new chief executive, said the company wants to reach $20 billion in assets within five years.

“You could say we're a niche player because I think that’s just the thing people say about companies that are our size. But we work with wealth advisors. We work with breakaway brokers. We do a significant amount of business with TAMPs (turnkey asset management programs),” says Maiorano, who previously helped expand RIA business at Nuveen Investments and at Schwab before taking over at Trust Company in January. “Four years ago I would say we were a small fledgling custodian. Now we actually have presence and we have significance in the marketplace. We don’t have to grow, but absolutely we want to grow.”

Indeed, for small custodians, growth should be deliberate and strategic. Peter Mangan, president and chief executive at Shareholders Service Group in San Diego, Calif., says he’s not looking to expand the firm aggressively. Mangan helped found the company in 2002 and today it manages several billion dollars in assets and growth of 20 percent to 30 percent a year. That’s not bad. “The pace of growth has been fairly steady over the past years. We don’t do a lot of marketing. We're really not aiming at becoming a real fast grower and looking for a quick exit. We enjoy the business and would like to run it for a long, long time to come,” Mangan says. “You can do more marketing and sales and increase the rate of growth, but you better be able to service it because if you don’t, you’ll just end up losing your credibility and losing your reputation.”

With the collapse of major investment banks following the credit meltdown of 2008, and the Bernard Madoff scandal, credibility is one of the qualities that advisors continue to seek from custodians. They want to know that their client’s money is safe. In this area, big firms with brand names may offer a certain comfort that smaller, lesser-known companies simply cannot. Perhaps that is at least in part why Schwab was rated the No. 1 custodian platform in a Morgan Stanley RIA survey released Feb. 1, getting 35 percent of advisor respondents’ votes. Fidelity was second, with 18 percent of the vote. The survey showed that 24 percent felt reputation was the most important factor in choosing a custodian, although a greater number of respondents rated other criteria — including service, technology platforms, and cost — as most important. “It has definitely become a critical question for investors to ask. Where’s my money, and how do I know it’s safe?” Mangan says.

On the other hand, credibility may be measured less by the amount of assets managed by a custodian than by the experience of the managers who are running the company, Mangan adds, and this can work to a smaller custodian’s advantage. “At the end of the day it’s a confidence issue,” he says. “Do advisors have confidence in your ability to deliver what they need to run their business? Not everybody does. You can see cases where firms have set up advisor businesses and decided it wasn’t worth it because they didn’t get the assets. Why didn’t they get the assets? It’s because the advisors are running their own businesses and they're not going to put those assets into the hands of someone who doesn’t know how to do what they’re doing, or who the advisors don’t trust will be there the next year and the year after.”

Sometimes an advisor will sign on with a smaller custodian simply because the advisor has difficulty setting up a relationship with a major player. Take Paul Acker, who started NetWorth Consulting in Washington state about 18 months ago and now manages around $5 million in assets. Acker says he decided to work with Shareholders Service Group after talks with a few of the larger ones, including TD Ameritrade, fell through. Acker said he was put off when the TD rep pressed him for a business plan and for AUM growth goals for the first year. He didn’t think he could grow as rapidly as they wanted him to. TD Ameritrade doesn’t require a prospective client to meet minimum asset levels, says Tom Nally, managing director of institutional sales, but it does expect advisors to demonstrate they want to run a growing business. “You don’t want to devote resources to somebody who’s not serious,” Nally says.

Shareholders Service Group’s Mangan said his company has no minimum AUM levels for advisors, but it does expect its advisors to be registered, have a corporate structure, and have client agreements. Acker met those criteria, and was “thoughtful and coherent about his plans for growth,” he adds. Mangan doesn’t worry too much about working with advisors who others may feel are too small to operate effectively. “The natural effect of running a business will weed out those that can’t sustain us or themselves. We don’t need to throw people out. The business environment takes care of that.”

Acker says he’s happy with his custodian and believes the relationship will thrive in the days ahead. “They probably don’t make money off me, but they know if my business grows, we’ll use more of their services,” he says.

close

For The Record

(source: Registered Rep)

March 1, 2010 — The Basics on the Custodians, Large and Small read more at Registered Rep »

The Online Wager

(by Christina Mucciolo, Registered Rep)

January 1, 2010 — Hedge fund manager Joel Greenblatt and online brokerage pioneer Blake Darcy recently opened an online managed account service for retail investors. Can Greenblatt’s star power take asset management online? more

In May, prominent hedge fund manager Joel Greenblatt and online brokerage pioneer Blake Darcy rolled out their online managed account service for retail investors called Formula Investing. They're not the first to try managed investing on the web. A handful of online managed account firms launched in the 1990s, but the model never quite caught on. Could Greenblatt’s star power attract more interest this time around? Some say, yes.

Not everyone in the financial services industry knows Greenblatt, but to those in the value investing game his name should sound very familiar. Now 52, he first rose to prominence as the manager of hedge fund Gotham Capital, which reports posting average annual returns of 40 percent over 20 years. But what really launched him as a value investing guru was his bestselling book, The Little Book That Beats the Market. Published by Wiley in 2005, that book laid out the simple long-term value investing strategy behind Formula Investing, and behind the free online stock-screen service “Magic Formula Investing” that preceded it. (In the simplest of terms, Greenblatt’s magic formula recommends putting together a concentrated portfolio of stocks that have both high earnings yield and high return on capital.)

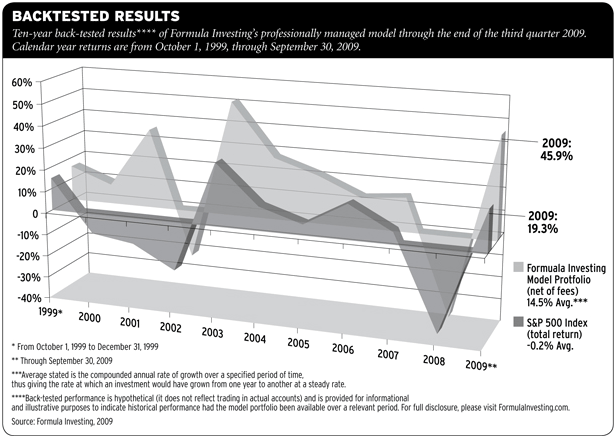

Within a few years, Greenblatt had legions of followers and dozens of blogs tracking the formula’s performance. Had you followed this formula between 1988 and 2004, you'd have earned an annualized return of 31 percent, more than double the return on the S&P 500.

Some analysts and industry insiders think Formula’s online model holds tremendous appeal, and predict that other investment managers and financial advisors will soon follow Greenblatt’s lead onto the web. Online managed accounts fill a gap in the market, catering to investors who fall somewhere on the continuum between strict do-it-yourselfers and those who want full-on comprehensive wealth management advice. And the web-based model makes it easy to build scale, something that many RIAs struggle with in the high-touch personal advice business.

“Marrying this online brokerage idea with the advice component is not a bad one,” says Aite Group analyst Alois Pirker. “There are a couple of things that play into that. With the crisis, clients still need advice, but they want to see their assets, so having an online capability is an added bonus.”

Of course, there are detractors, too, who say Greenblatt’s investing strategy could underperform, that back-tested results are useless, that he charges too much, and that most investors really want a face-to-face relationship.

Thinking Big

Whatever the outcome, Greenblatt and Darcy have big ambitions. The duo officially launched Formula Investing in October, and Darcy says that within five years, they expect to be managing “billions” of assets. So far, through mid-December, the firm has accumulated $25 million in a couple hundred accounts (they declined to be more specific). That’s not a bad start. “This is not meant to be a little niche business,” says Darcy. “We constructed it so it can be leveraged up in a very large way.” Darcy, who started one of the first online brokerages, DLJdirect, back in 1987, is a strong believer in the web. “One of the next waves of change in the financial services industry is a movement towards more being done in the online world, that is customers going directly into money management products on the web, where managers will communicate via webcast,” he says. “That is going to happen. The tools are increasingly getting there.”

Formula itself offers paperless account opening, an e-sign in for customers, online performance reporting, real-time access to account holdings and a way for customers to communicate with the managers through email. Its portfolios are truly customized — clients can select individual stocks they don’t want to hold. They are also as liquid as a mutual fund, and rebalanced quarterly. Formula charges a one percent annual asset-based fee, which includes all transaction costs, with breakpoints at $1 million and $10 million. The account minimum is $25,000 for the first account, and $5,000 for each additional account, but the average account holds around $60,000.

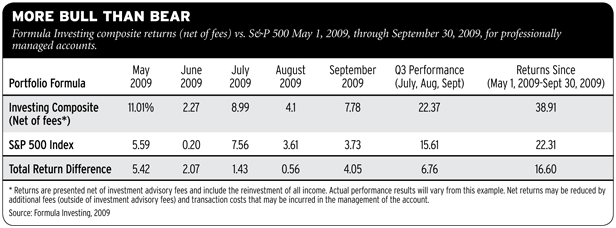

Greenblatt’s investing strategy is simple. The firm rates the 3,500 largest companies traded on U.S. stock exchanges based on its own calculations of two popular metrics — return on capital and earnings yield — and the companies with the best combined scores are selected for the portfolio. Formula Investing actually offers a self-managed account option, where investors can decide how many stocks they want to buy, and can pick individual stocks from Greenblatt’s list, but these clients correspond to just 5 percent of accounts at this point. The other 95 percent have opted for the fully managed version of Formula Investing, which starts off with the 24 stocks that receive the best ranking according to their formula. Once a quarter for the first year, the bottom ranked six stocks from what remains of that original portfolio of 24 are sold, and the top ranked six stocks in the universe of 3,500 stocks that aren’t already in the portfolio are bought to replace them. The following year, they begin to sell securities when they have been held for a year. They also begin to manage the portfolio for tax-efficiency, harvesting tax losses just before the one-year mark and gains just after the one-year mark. Of course, Formula Investing hasn’t been operating long enough to have an established track record, but between May and September 30, the Formula Investing portfolios outperformed the S&P 500 by 16.60 percent, according to composite results.

Formula Investing has no intention of cutting out the middle man. The firm plans to roll out its managed service to RIAs in the first quarter, either serving as an outside manager or a select manager on platforms like Lockwood Advisors and Envestnet. For subadvisory accounts, Darcy says Formula will charge 50 basis points or less. (For some cost perspective, according to Morningstar, fees for an active separate account average around 71 basis points, and passive separate account fees average 13 basis points.) The firm also plans to roll out other managed portfolios online. Some long-short strategies have been running in accounts since June, and Darcy says they will begin offering these to clients in the first quarter, when they will also launch an international strategy portfolio.

Will advisors bite? Darcy says the firm has already spoken to a number of interested advisors. But its appeal may depend in part on its performance in the next year. “I do think advisors will be interested in it,” says Jason Wenk, founder and principal of RIA Retirement Strategies. “The reality is if it performs well, then who cares where it came from. But I do think a certain number of semi-lazy advisors would like to position themselves alongside an expert.”

Onto The Web

Some analysts and financial advisors agree with Darcy that the migration of money management onto the web is inevitable. With costs rising, and asset levels falling, RIAs are trying to increase scale these days, which can be difficult to do in a business that requires a lot of face time with each individual client, says Aite’s Pirker. Putting the web between the expert and the client could partially solve this problem.

But there is an element in Greenblatt’s model that could be difficult for the everyday advisor or money manager to replicate: celebrity. “What he is playing off of as well is social networking,” says Pirker. “You have this public personality and reputation, and how can you leverage that in the industry. You want to scale that reputation further, be able to service more business with that.”

There are already a number of self-directed investing websites that attempt to harness the celebrity of other famous investors, or have a social networking component. AlphaClone, cofounded by Cambria Investment Management portfolio manager Mebane Faber, allows investors to research and mimic the performance of the world’s best hedge fund managers and institutional investors by tracking their holdings at the website. And online portfolio sharing service Covestor, launched in 2008, offers a variation on this theme. Individual self-directed investors and established managers can throw their own portfolios up on the site, which tracks each portfolio’s performance. The individual managers can then charge other users fees to follow their investment decisions in real time. kaChing, launched in October 2009, offers an almost identical service and already boasts 400,000 users — both on their website and through applications on Facebook, Yahoo, and the iPhone.

There are also a handful of websites that recommend model portfolios for a fee. One such website is FolioFN, which offers Folio Investing, an online trading and investing service through which investors can buy “Ready-to-Go-Folios” that are built around a particular investing strategy.

Interest in online managed accounts seems to be growing, according to Jagdish Rangwani, chief operating officer of iNautix, a division of Pershing, which built the custom-made client web portal Formula Investing is using. He says a number of advisors who wanted to begin offering clients accounts online approached the firm in the second half of 2009. “This is almost like a new breed of advisors who are coming into the market to offer these services online, and not in a traditional way,” says Rangwani. “They have some investment models that they want to offer to their customers and they want to build this whole thing online.”

Michael Edesess, partner and chief investment officer at RIA Fair Advisors, author of The Big Investment Lie, published in 2007 by Berrett-Koehler, and a Ph.D. in math, is one advisor who is considering a move onto the web. He and his partner already offer traditional personalized face-to-face advice, but are planning to add an online advice component next year when they have worked the kinks out of their program and ironed out legal issues.

“The main business challenge is how to serve clients at low cost to them while including just enough of the personal element of service to cater to the client’s preferences,” says Edesses. “Some clients really want a lot of face time and hand holding, but many only need to know that their advisors are knowledgeable, wise and honest and are truly pursuing their interests. Once they are satisfied on these accounts they will be happy with an automated or semi-automated service — and it will consume less of their valuable time too. We would mostly expect it to draw new clients, though of course we’ll let existing clients know about it.”

The Challenge

Of course, not everyone thinks Formula Investing will be a game changer for the investment management industry. If Greenblatt’s investment strategy blows up on him, the whole thing would be kaput, say a few detractors. Despite his own interest in the online advice model, Edesses thinks Greenblatt’s model relies too heavily on a blind faith in value investing. “Back-tested results tell you nothing,” he says. “It is an ironclad rule that whatever strategy outperformed the market in the past — after adjusting for risk — cannot be expected to do so in the future. Unless the ‘value investing’ strategy — Greenblatt’s strategy — somehow eludes this rule it will not succeed in the future.”

Greenblatt himself admits that the strategy will have its down years, and says that in order for it to work for investors they will have to be willing to stick it out for the long-term. But his critics predict that most clients will not have the fortitude to do that, especially without a strong personal relationship with a financial advisor to keep them on track. “I'm curious to see how that business model performs when he goes through an underperforming period,” says Scott Schermerhorn of RIA Granite Investment Advisors.

And then there are those who worry that because of the transparency of his strategy, he will be front-run by other investment managers or traders. Greenblatt’s response? Most quants are looking for short-term gains or consistent monthly annual returns, while Formula’s strategy rewards long-term investors. Darcy also says that it is harder to front-run than it might seem. Though the free do-it-yourself service does offer you a list of stocks to invest in, they are presented to investors in alphabetical order rather than in order of ranking. Whoever wanted to copy the strategy exactly would have to come up with their own formulas for calculating earnings yield and return on capital for each stock on the list. “There are a number of ways you calculate these things,” says Darcy. And they do not share their secret.

close